1. Introduction

Money is one of the most important enablers in our lives, whether it is for buying a home, funding higher education, starting a business, or handling unexpected emergencies. However, we do not always have the required funds available at the exact time we need them. This is where loans play a crucial role. A loan allows an individual or business to borrow money with the promise of repayment over time, usually with interest.

Loans are not just about borrowing money—they are about creating opportunities. They help families build their dream homes, students pursue world-class education, and entrepreneurs expand their businesses. At the same time, loans require careful planning, as poor repayment discipline can lead to financial stress.

In this comprehensive blog, we will cover everything you need to know about loans—from their meaning and types to the advantages, risks, myths, and best practices for responsible borrowing. Whether you are a first-time borrower or someone exploring different financing options, this guide will give you the clarity you need to make informed financial decisions.

2. Basics of Loans

At its core, a loan is a financial agreement between a lender (such as a bank, credit union, non-banking financial company, or digital lending platform) and a borrower (an individual, business, or institution). The lender provides a certain amount of money, called the principal, which the borrower agrees to repay over a specified period, usually with interest.

Understanding the key components of a loan is essential for anyone planning to borrow:

a) Principal

The principal is the original sum of money borrowed. For example, if you take a loan of ₹5,00,000 to buy a car, the ₹5,00,000 is your principal amount.

b) Interest

Interest is the cost of borrowing money. It is usually expressed as a percentage of the loan amount (interest rate) and is paid to the lender in exchange for providing the funds.

c) Tenure

Loan tenure is the period over which the loan is to be repaid. It can range from a few months (for personal loans) to 20–30 years (for home loans).

d) EMI (Equated Monthly Installment)

Most loans are repaid in EMIs. An EMI includes both principal and interest portions, spread out evenly across the loan tenure. This makes repayment more manageable for borrowers.

e) Secured vs. Unsecured Loans

- Secured loans are backed by collateral, such as property, gold, or fixed deposits. Because the lender’s risk is lower, secured loans often have lower interest rates.

- Unsecured loans do not require collateral. Examples include personal loans and credit card loans. Since the lender carries more risk, the interest rates are usually higher.

f) Fixed-Rate vs. Floating-Rate Loans

- Fixed-rate loans have a constant interest rate throughout the tenure, offering predictability in EMIs.

- Floating-rate loans (also called variable-rate loans) change based on market conditions, which means EMIs can go up or down over time.

g) Other Charges

In addition to interest, loans may come with processing fees, prepayment charges, foreclosure penalties, and late payment fees. Borrowers should always consider these hidden costs before signing a loan agreement.

👉 Understanding these basics ensures that borrowers know exactly what they are getting into, avoiding confusion and future financial stress.

3. Major Types of Loans

Loans come in many forms, each designed to meet specific financial needs. Knowing the different types of loans can help you choose the right option for your situation. Below are the most common loan categories explained in detail:

a) Personal Loans

- Definition: An unsecured loan that can be used for almost any purpose, such as medical emergencies, weddings, vacations, or debt consolidation.

- Key Features:

- No collateral required

- Flexible usage

- Shorter tenure (usually 1–5 years)

- Higher interest rates compared to secured loans

- Best for: Urgent or unplanned expenses when you don’t want to pledge any asset.

b) Home Loans

- Definition: A secured loan taken to purchase, construct, or renovate a house.

- Key Features:

- Collateral: The property itself

- Long tenure (up to 30 years)

- Relatively low interest rates

- Offers tax benefits on both principal (under Section 80C) and interest payments (under Section 24 of the Income Tax Act in India)

- Best for: Individuals looking to buy or build a home without exhausting their savings.

c) Car Loans (Auto Loans)

- Definition: A secured loan provided to finance the purchase of a car, bike, or other vehicle.

- Key Features:

- Collateral: The vehicle purchased

- Medium tenure (3–7 years)

- Competitive interest rates

- EMI starts soon after disbursement

- Best for: People who want to buy a vehicle without paying the entire cost upfront.

d) Education Loans

- Definition: A loan designed to cover tuition fees, living expenses, and other costs of higher education in India or abroad.

- Key Features:

- Collateral required for higher loan amounts

- Moratorium period (repayment starts after studies + grace period)

- Interest subsidy schemes for eligible students

- Best for: Students and families investing in higher education without liquidating savings.

e) Business Loans

- Definition: Loans specifically for entrepreneurs and business owners to fund working capital, expansion, or machinery purchase.

- Key Features:

- Can be secured (backed by assets) or unsecured

- Flexible repayment terms

- Offered by banks, NBFCs, and new-age fintech lenders

- Best for: Small and medium businesses (SMEs), startups, and established firms looking for growth funding.

f) Gold Loans / Secured Loans

- Definition: A loan taken against gold jewelry or coins, where the borrower pledges gold as collateral.

- Key Features:

- Quick approval and disbursement

- Lower interest rates compared to personal loans

- Loan amount depends on the value of gold pledged

- Best for: Individuals needing instant cash for emergencies with minimal documentation.

g) Microfinance Loans

- Definition: Small loans offered to low-income individuals or groups, often without collateral, to promote financial inclusion.

- Key Features:

- Typically given to women or self-help groups (SHGs)

- Small ticket size (a few thousand to lakhs)

- Short repayment cycles

- Best for: Rural entrepreneurs, small traders, and self-employed individuals.

h) Government-Subsidized Loans

- Definition: Loans provided under government schemes to promote sectors like agriculture, housing, small businesses, and education.

- Examples in India:

- PMAY (Pradhan Mantri Awas Yojana): Subsidized home loans

- Mudra Loans: For small businesses and startups

- Kisan Credit Card (KCC): For farmers to meet crop-related expenses

- Best for: Individuals who qualify for government schemes and want affordable financing options.

👉 The diversity of loan options ensures that whether you’re a student, a salaried employee, a business owner, or a farmer, there is a loan product tailored to your financial requirements. The key is to select the right type that matches your goals and repayment ability.

4. How Loans Work

A loan might seem simple—you borrow money and repay it over time. However, there’s a structured process behind it, and understanding this mechanism helps borrowers make better financial decisions.

Here’s a breakdown of how loans work:

a) Loan Application Process

- Application Submission:

The borrower submits a loan application to the lender (bank, NBFC, or digital platform), providing details such as purpose, income, employment, and repayment capacity. - Documentation:

Commonly required documents include:- Identity proof (Aadhaar, Passport, etc.)

- Address proof

- Income proof (salary slips, bank statements, ITRs)

- Collateral documents (if applicable, like property papers or gold certificates)

- Verification & Credit Check:

Lenders verify the documents and check the applicant’s credit score (CIBIL score in India, FICO score globally) to assess repayment history and financial discipline. - Loan Approval:

If eligibility criteria are met, the lender approves the loan and issues a sanction letter with terms and conditions. - Disbursement:

The sanctioned loan amount is transferred to the borrower’s bank account or directly to the service provider (e.g., to a car dealer in case of auto loans).

b) Eligibility Criteria

While requirements vary by loan type and lender, common factors include:

- Age (usually 21–60 years for individuals)

- Employment stability or business track record

- Income level and repayment capacity

- Credit score (a higher score means better approval chances and lower interest rates)

- Collateral value (for secured loans)

c) Credit Score Importance

Your credit score is one of the most important factors in loan approval.

- A score of 750+ is generally considered excellent.

- A higher score increases chances of approval and favorable terms.

- Poor scores may lead to rejection or higher interest rates.

Maintaining a good credit history by paying bills, EMIs, and credit card dues on time is essential.

d) Interest Calculation

There are two main methods lenders use to calculate interest:

- Simple Interest:

- Formula: (Principal × Rate × Time) / 100

- Example: A ₹1,00,000 loan at 10% simple interest for 1 year = ₹10,000 interest.

- Compound Interest (common in loans):

- Interest is calculated on both the principal and the accumulated interest.

- This increases the total repayment amount compared to simple interest.

Most retail loans like personal, home, and car loans use compound interest with monthly reducing balance.

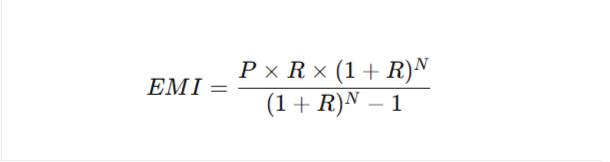

e) EMI (Equated Monthly Installment) Calculation

EMI is the fixed amount a borrower pays every month until the loan is repaid.

Formula:

Where:

- P = Loan amount (Principal)

- R = Monthly interest rate (Annual Rate ÷ 12 ÷ 100)

- N = Tenure in months

Example: For a ₹5,00,000 loan at 10% annual interest for 5 years (60 months), the EMI ≈ ₹10,624.

Online EMI calculators provided by banks and fintech apps make it easier for borrowers to estimate repayments.

f) Repayment & Foreclosure

- Borrowers repay through EMIs over the tenure.

- Some lenders allow prepayment (partial extra payment) or foreclosure (closing the loan early) with or without charges.

- Early repayment reduces interest burden but must be balanced with any penalties.

👉 In simple terms, a loan is not just about receiving money—it’s about eligibility, cost of borrowing, and repayment planning. Borrowers who understand this process are more likely to avoid debt traps and build a healthy financial profile.

5. Pros and Cons of Taking Loans

Taking a loan can be a smart financial decision when managed wisely, but it also carries potential risks if not handled responsibly. Understanding both sides of borrowing helps individuals and businesses decide when a loan is a tool for growth versus when it might become a financial burden.

✅ Pros of Taking Loans

- Financial Flexibility

Loans provide access to funds when you don’t have enough savings. Whether it’s buying a house, paying for higher education, or covering medical emergencies, loans bridge the financial gap. - Asset Creation

Loans enable individuals to build valuable assets like homes or vehicles without waiting years to save the entire cost. Businesses can also invest in machinery, infrastructure, or expansion. - Emergency Support

In urgent situations—such as hospitalization or unforeseen expenses—a quick loan can provide much-needed relief without liquidating long-term investments. - Boosting Credit Profile

When repaid on time, loans improve credit history and increase credit scores, making it easier to borrow in the future at better interest rates. - Tax Benefits

Certain loans, like home loans and education loans, provide tax deductions on interest payments, reducing overall financial burden. - Business Growth & Opportunities

For entrepreneurs, business loans provide working capital to seize opportunities, scale operations, and remain competitive.

❌ Cons of Taking Loans

- Debt Trap Risk

Over-borrowing or taking multiple loans at high interest rates can lead to a debt trap, where most of your income goes into EMIs. - Interest Burden

Even though loans give instant access to funds, the repayment includes not just the principal but also significant interest, which can sometimes double the original cost over long tenures. - Credit Score Impact

Missing EMIs or defaulting on a loan severely damages your credit score, reducing chances of approval for future loans or credit cards. - Collateral Risk (for Secured Loans)

In secured loans, failure to repay may result in losing the asset pledged (house, gold, or vehicle), which can cause both financial and emotional distress. - Hidden Charges

Many loans come with processing fees, late payment penalties, foreclosure charges, and insurance requirements that increase the overall cost of borrowing. - Psychological Stress

Continuous debt repayment can cause stress and anxiety, especially if income is unstable or unexpected financial challenges arise.

👉 Balanced View:

Loans are neither inherently good nor bad—they are financial tools. When used strategically (for education, housing, or business growth), loans can create long-term benefits. But when used carelessly (impulsive spending, frequent borrowing), they can lead to financial instability.

6. Factors to Consider Before Borrowing

Borrowing money is a serious financial decision. While loans can provide quick access to funds, the wrong choice can lead to long-term stress. Before signing any loan agreement, carefully evaluate these factors:

a) Purpose of the Loan

Clearly identify why you need the loan. Is it for an asset (like a house or car), education, medical emergency, or business growth? Borrowing for productive purposes (asset creation, career investment) is often wiser than borrowing for lifestyle expenses.

b) Loan Amount Needed

Avoid the temptation to borrow more than necessary. Excess funds may give short-term comfort but increase your interest burden and repayment pressure.

c) Repayment Capacity

Assess your monthly income and expenses realistically. A safe guideline is to ensure that your total EMIs (existing + new loan) do not exceed 35–40% of your net monthly income. This keeps your budget balanced and leaves room for savings.

d) Interest Rates & Total Cost of Borrowing

Do not just focus on the advertised interest rate. Compare the Annual Percentage Rate (APR), which includes processing fees, insurance, and other charges. Sometimes a “low-interest” loan may turn out more expensive once hidden costs are added.

e) Loan Tenure

- Short Tenure: Higher EMIs but lower total interest outgo.

- Long Tenure: Lower EMIs but significantly higher total interest.

Choose a tenure that balances affordability with long-term cost efficiency.

f) Type of Loan: Secured vs. Unsecured

- Secured loans (home loan, gold loan, car loan) offer lower interest but require collateral.

- Unsecured loans (personal loans, credit card loans) don’t need collateral but charge higher interest.

Select based on your risk comfort and financial situation.

g) Credit Score Impact

Your credit score affects both approval chances and interest rates. A higher score (750+) gives you better negotiating power. If your score is low, work on improving it before applying.

h) Prepayment & Foreclosure Rules

Check if the lender allows you to repay early without heavy penalties. Being able to prepay reduces interest costs if you get surplus income in the future.

i) Terms & Conditions

Always read the fine print carefully. Look for:

- Hidden charges

- Late payment penalties

- Collateral seizure clauses (for secured loans)

- Mandatory insurance add-ons

👉 Bottom Line: Borrowing can be financially empowering if done wisely. The right loan, taken with proper planning, supports your goals without harming your financial stability.

7. Loan Myths vs. Reality

Loans are surrounded by several misconceptions that often mislead borrowers. Believing these myths can result in poor financial decisions, unnecessary stress, or missed opportunities. To borrow wisely, it’s important to separate myths from facts.

✅ Common Loan Myths and the Truth Behind Them

1. Myth: Loans are only for people in financial trouble.

- Reality: Loans are financial tools, not last-resort solutions. Businesses use loans for expansion, students for education, and families for home purchases. Borrowing smartly can help build assets and improve one’s standard of living.

2. Myth: Taking a loan ruins your credit score.

- Reality: Simply having a loan does not harm your credit score. In fact, timely repayment improves your credit history. It’s only missed or delayed payments that negatively affect your score.

3. Myth: The lowest interest rate means the best loan.

- Reality: While low interest is attractive, other factors matter—processing fees, penalties, prepayment charges, and hidden costs. A slightly higher rate loan with flexible terms might be more beneficial.

4. Myth: You must always borrow from your primary bank.

- Reality: Many non-banking financial companies (NBFCs), fintech platforms, and credit unions offer competitive loan products. Comparing multiple lenders helps secure better deals.

5. Myth: Only people with high income can get loans.

- Reality: Loan approval depends on multiple factors—credit score, repayment ability, collateral (for secured loans), and lender’s policies. Even moderate-income individuals can qualify for appropriate loans.

6. Myth: Prepaying a loan is always penalty-free.

- Reality: Some lenders charge foreclosure or prepayment fees to compensate for interest loss. Always check the terms before planning early repayment.

7. Myth: Online loans are unsafe.

- Reality: While fraudulent platforms exist, most regulated digital lending platforms are safe, transparent, and convenient. Borrowers just need to ensure the lender is RBI-registered or licensed in their jurisdiction.

💡 Key Takeaway

Believing loan myths can lead to hesitation, overpaying, or even avoiding opportunities. By understanding the facts, borrowers can make smarter, more confident financial decisions.

8. How to Manage Loans Smartly

Taking a loan is only the first step; managing it wisely is what ensures financial stability and long-term peace of mind. Poor handling can lead to mounting debt, while smart strategies can help you clear loans faster and improve your credit score.

✅ Smart Loan Management Tips

1. Create a Repayment Plan

- Set up a budget that includes your EMIs as a fixed expense.

- Prioritize loan payments over discretionary spending to avoid penalties.

2. Pay EMIs on Time

- Timely payments protect your credit score and reduce financial stress.

- Setting up auto-debit or reminders ensures you never miss due dates.

3. Avoid Taking Multiple Loans Unnecessarily

- Having too many active loans increases debt burden and makes repayment difficult.

- Stick to essentials and avoid borrowing for non-urgent needs.

4. Consider Making Part-Payments

- Whenever you receive bonuses, incentives, or extra income, use part of it to reduce the outstanding loan amount.

- This lowers the overall interest paid.

5. Refinance or Balance Transfer if Needed

- If you find a lender offering lower interest rates or better terms, consider transferring your loan.

- However, check for hidden charges before making the switch.

6. Maintain a Healthy Credit Score

- Good credit opens doors to better loan terms in the future.

- Avoid defaulting and keep your credit utilization ratio under control.

7. Build an Emergency Fund

- An emergency fund covering at least 3–6 months of EMIs ensures you don’t default in case of job loss or unexpected expenses.

8. Avoid Minimum Payments on Credit Loans

- Paying only the minimum due on credit cards or personal loans leads to high interest accumulation. Always aim to pay in full.

💡 Key Takeaway

Managing loans smartly requires discipline, planning, and consistent repayment. With the right approach, loans can be a stepping stone toward financial growth instead of a burden.

9. Latest Trends in the Loan Industry

The loan industry is evolving rapidly with technology, changing consumer behavior, and innovative financial models. Staying updated on the latest trends helps borrowers make informed decisions and lenders offer better services.

🔑 Key Trends Shaping the Loan Industry

1. Digital Lending Platforms

- Online loan applications and instant approvals are becoming the norm.

- Borrowers now enjoy a seamless experience without lengthy paperwork.

2. AI and Machine Learning in Credit Scoring

- Traditional credit scores are being supplemented by AI-driven risk assessments.

- Alternative data like utility bills, rent payments, and spending patterns are now considered for loan eligibility.

3. Rise of BNPL (Buy Now, Pay Later)

- Short-term micro-loans through BNPL services are popular among millennials and Gen Z.

- They offer convenience for online shopping with flexible repayment options.

4. Peer-to-Peer (P2P) Lending

- Platforms connecting borrowers directly with individual investors are gaining popularity.

- This trend makes borrowing more accessible and often at competitive rates.

5. Green Financing & Sustainable Loans

- Loans for eco-friendly projects such as solar energy, electric vehicles, and sustainable housing are on the rise.

- Banks and NBFCs are offering lower interest rates for green initiatives.

6. Blockchain & Smart Contracts

- Blockchain ensures transparency and security in loan agreements.

- Smart contracts automate loan disbursal and repayment, reducing fraud risks.

7. Personalization of Loan Offers

- Lenders use big data to tailor loan products to individual borrower needs.

- This leads to better customer experiences and responsible lending.

8. Regulatory Advancements

- Governments and financial regulators are strengthening guidelines on digital lending to protect consumers from fraud and predatory practices.

💡 Key Takeaway

Technology is reshaping the loan industry, making borrowing faster, safer, and more personalized. For borrowers, staying aware of these trends ensures smarter financial decisions.

10. Conclusion

Loans are powerful financial tools that can help individuals and businesses achieve their goals—whether it’s buying a home, pursuing higher education, expanding a business, or managing emergencies. However, borrowing always comes with responsibility.

Understanding the basics of loans, types, working mechanisms, pros and cons, myths, and industry trends ensures that borrowers make informed and confident financial decisions.

A well-planned loan can be a stepping stone to growth, but careless borrowing can lead to debt traps. The key lies in evaluating your repayment capacity, financial goals, and long-term stability before signing any agreement.

💡 Final Thought: Borrow wisely, repay responsibly, and use loans as a tool to secure—not compromise—your financial future.